Market Backdrop

U.S. equity markets enter 2026 with a setup that has historically created compelling opportunities for disciplined investors. Leadership within U.S. equities remains narrow and expensive, dominated by large-cap growth stocks trading at elevated valuation multiples. In contrast, small-cap equities offer historically attractive valuations and a favorable setup for potential outperformance.

The top ten companies by market capitalization in the S&P 500 Index (S&P 500) now represent 41.1% of the index, while the top ten by earnings represent 32.6% of the index. This concentration is not only narrow, but it is also expensive, with the top ten by weight in the S&P 500 trading at an average of 29 times forward earnings, compared to 19 times for the remaining 490 constituents.

Valuation gaps between value and growth, as well as between small caps and large caps, remain near historical extremes based on nearly all metrics. The Russell 1000 Value Index’s 17 times forward price-to-earnings (P/E) ratio is trading at a 40% discount compared to the Russell 1000 Growth Index’s 29 times P/E, one of the largest discounts since the early 2000s (see following chart).

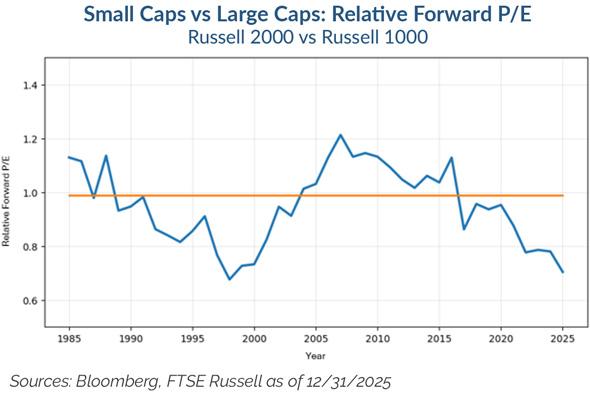

Similarly, small caps, represented by the Russell 2000 Index, trade at substantial discounts relative to large caps, Russell 1000 Index, including a roughly 30% discount on forward price-to-earnings (see chart below), a 57% discount on price-to-book, and a 44% discount on enterprise value to free cash flow. These valuation disparities underscore the breadth of opportunity within the small-cap universe.

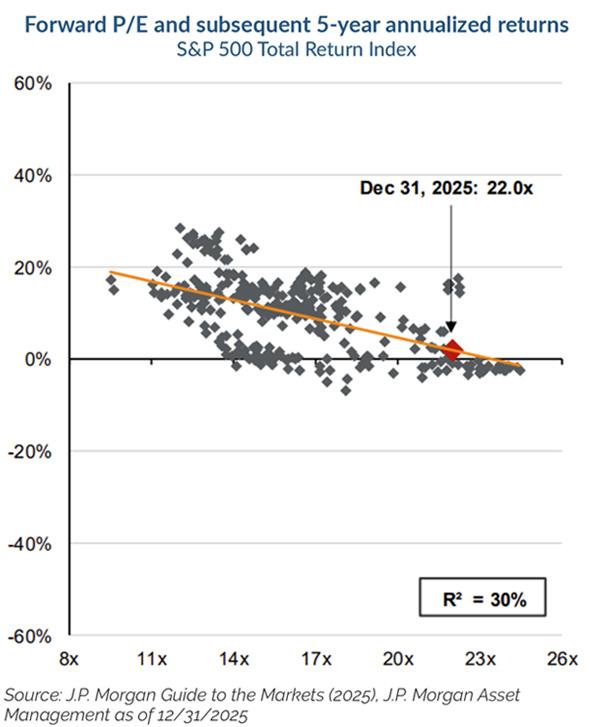

The current market environment bears resemblance to the late 1990s in terms of this growth-to-value, large-to-small disparity. We anticipate mean reversion in the price/earnings multiples commanded by large-cap and artificial intelligence-related stocks relative to small-cap value, although we acknowledge this process can unfold gradually. In our late-1990s analogy, this took approximately two years to fully inflect but ultimately lasted over seven years. With the S&P 500 trading at 22 times forward earnings amid historically narrow leadership, we believe this presents an actionable opportunity for small-cap value equities today, offering higher forward return potential with lower embedded expectations and better asymmetrical payouts. JPMorgan Chase & Co. notes forward five-year annualized S&P 500 total returns are quite low when past multiples have been this high (see chart below).

Concentration risk remains a challenge for large-cap growth investors as index leaders are priced for near-perfection and require elite execution to meet already high embedded expectations, with little margin for error. The catalyst for the re-rating in valuation will be multi-faceted, but it should occur as investors realign their future cash flow expectations with reported earnings. We expect the difference between expectations and reality will be disappointing.

With small-cap value equities generally overlooked by market participants for over a decade, we view the lack of attention to the asset class as a prime opportunity to identify mispricing and drive sustained outperformance over the next number of years. The exploitable market inefficiencies are pronounced in the small-cap space, where limited capital and sell-side analyst coverage enable our team to find mispriced opportunities with asymmetric risk/reward profiles.

With small-cap value equities generally overlooked by market participants for over a decade, we view the lack of attention to the asset class as a prime opportunity to identify mispricing and drive sustained outperformance over the next number of years.

2026 Market Dynamics

Monetary and fiscal policy dynamics are increasingly constructive for small-cap value. We expect additional interest rate cuts through 2026, although the market currently is not pricing these in until early second-quarter of 2026. Cuts could arrive sooner as leading economic indicators continue to weaken. Labor markets are likely to remain the primary driver of policy decisions, as the U.S. Federal Reserve Board (Fed) responds to layoffs and weakening employment conditions, with the goal of accelerating economic growth. Inflation has become a secondary issue for the Fed relative to jobs, and we believe fears of re-accelerating inflation are largely overblown as inflation has moderated.

Looking ahead, with Fed Chair Jerome Powell’s term expiring in May, we expect a Trump-appointed successor to pursue a more stimulative monetary policy overall. This shift may lead to a steepening yield curve, with the long end rising on expectations of higher growth and investor hesitancy to purchase long-term paper given the fiscal deficit and debt imbalances. We are closely watching this dynamic as it may prove challenging for mortgages. Notably, the Fed has recently resumed quantitative easing (QE), purchasing assets to help the cash markets. It is possible the Fed may extend these plans to mortgage-backed securities or 10-year Treasuries to lower mortgage rates, a potentially significant development that remains underdiscussed. This drift back toward the post-credit crisis QE playbook should be positive for the U.S. economy and risk assets in the near term.

Tax and trade measures enacted or extended by the current U.S. administration are expected to increasingly flow through to the real economy in 2026, disproportionately benefiting domestically focused small-cap value companies. We are also monitoring a U.S. Supreme Court case regarding the constitutionality of certain tariffs, which could introduce additional volatility in select industries.

Taken together, these dynamics favor many of the end markets and companies represented across our portfolio. Financials stand to benefit from a steepening yield curve, while Industrials, Materials, and Information Technology companies are well positioned for ongoing onshoring initiatives. Consumer Discretionary companies may benefit from a resilient U.S. consumer, and the Health Care sector has become an increasingly attractive area as demographic trends and policy developments create new opportunities.

As long-tenured contrarians, we maintain a cautious view of consensus sell-side forecasts and public sentiment, which appear to be generally positive. Geopolitical uncertainty remains elevated abroad while domestically, the current U.S. administration has shown a penchant for maneuvering outside of established norms.

Somewhat concerning is the proliferation of private credit. The recent emergence of fraud and credit deterioration has caused trouble for many investors and financial institutions. We are looking at this area of the market with great interest to make sure spillover effects stemming from lending and underwriting by non-expert participants are contained and manageable.

ncouragingly, we have begun to see instances of asset flows rotating back into value, and small-cap value equities specifically. We expect this to be an additional tailwind that supports small-cap value over the intermediate term, and we view today’s setup as the opportune time for small-cap active value exposure. Forces that have worked against small-cap value and active management for the last decade now represent a material go-forward opportunity. Specifically, fewer active participants and increased correlations across index constituents are providing even more avenues for our established process to identify mispricing and drive meaningful risk-adjusted returns.

Forces that have worked against small-cap value and active management for the last decade now represent a material go-forward opportunity.

IMPORTANT INFORMATION

© 2026. Easterly Asset Management. All rights reserved.

As of 6/30/2025, Easterly Asset Management (“Easterly”) and its Strategic Partners have $4.2B in managed assets which includes nearly $3B in AUM managed by Easterly’s wholly owned subsidiary, Easterly Investment Partners LLC, a registered investment adviser. Easterly serves as the growth platform for the firm’s asset management business. In 2021, Easterly formed Easterly Clear Ocean to take advantage of opportunities and dislocations in the international shipping markets. In November 2023, Easterly announced a strategic partnership with Lateral Investment Management where Easterly will provide access to its technology, fundraising, and operations expertise, and will invest alongside the firm in certain deals. In October 2024, Easterly acquired the ROC Municipals municipal bond team. EAB Investment Group and Orange Investment Advisors are subadvisors for certain investment strategies and mutual funds offered by Easterly; they are not directly affiliated with Easterly. Easterly Snow, Easterly Murphy, Easterly Ranger and Easterly ROC Municipals are investment teams of Easterly Investment Partners LLC, an SEC-registered investment adviser. EAB Investment Group LLC (d/b/a Easterly EAB), Orange Investment Advisors LLC (d/b/a Easterly Orange), and Lateral Investment Management are separate SEC-registered investment advisers that are strategic partners of Easterly. Each investment adviser’s Form ADV is available at www.sec.gov. Registration does not imply and should not be interpreted to imply any particular level of skill or expertise.

No funds or investment services described herein are offered or will be sold in any jurisdiction in which such an offer or sale would be unlawful under the laws of such jurisdiction. No such fund or service is offered or will be sold in any jurisdiction in which registration, licensing, qualification, filing or notification would be required unless such registration, license, qualification, filing, or notification has been effected.

The material contains information regarding the investment approach described herein and is not a complete description of the investment objectives, risks, policies, guidelines or portfolio management and research that supports this investment approach. Any decision to engage the Firm should be based upon a review of the terms of the prospectus, offering documents or investment management agreement, as applicable, and the specific investment objectives, policies and guidelines that apply under the terms of such agreement. There is no guarantee investment objectives will be met. The investment process may change over time. The characteristics set forth are intended as a general illustration of some of the criteria the strategy team considers in selecting securities for client portfolios. Client portfolios are managed according to mutually agreed upon investment guidelines. No investment strategy or risk management techniques can guarantee returns or eliminate risk in any market environment. All information in this communication has been obtained from sources believed to be reliable but cannot be guaranteed. Investment products are not FDIC insured and may lose value.

Investments are subject to market risk, including the loss of principal. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate. The information contained herein does not consider any investor’s investment objectives, particular needs, or financial situation and the investment strategies described may not be suitable for all investors. Individual investment decisions should be discussed with a personal financial advisor.

Any opinions, projections and estimates constitute the judgment of the portfolio managers as of the date of this material, may not align with the Firm’s opinion or trading strategies, and may differ from other research analysts’ opinions and investment outlook. The information herein is subject to change without notice and may be superseded by subsequent market events or for other reasons. Easterly assumes no obligation to update the information herein.

References to securities, transactions or holdings should not be considered a recommendation to purchase or sell a particular security and there is no assurance that, as of the date of publication, the securities remain in the portfolio. Additionally, it is noted that the securities or transactions referenced do not represent all of the securities purchased, sold or recommended during the period referenced and there is no guarantee as to the future profitability of the securities identified and discussed herein. As a reminder, investment return and principal value will fluctuate.

The indices cited are, generally, widely accepted benchmarks for investment performance within their relevant regions, sectors or asset classes, and represent non managed investment portfolio. It is not possible to invest directly in an index.

This communication may contain forward-looking statements, which reflect the views of Easterly and/or its affiliates. These forward-looking statements can be identified by reference to words such as “believe”, “expect”, “potential”, “continue”, “may”, “will”, “should”, “seek”, “approximately”, “predict”, “intend”, “plan”, “estimate”, “anticipate” or other comparable words. These forward-looking statements or other predications or assumptions are subject to various risks, uncertainties, and assumptions. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. Should any assumptions underlying the forward-looking statements contained herein prove to be incorrect, the actual outcome or results may differ materially from outcomes or results projected in these statements. Easterly does not undertake any obligation to update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by applicable law or regulation.

Past performance is not indicative of future results.

20260123_5152827