The third quarter of 2024 (Q3 2024) marked a significant, yet anticipated change to the Federal Reserve’s (the Fed) monetary policy outlook. In September, the U.S. central bank cut its benchmark interest rate by half a percentage point and signaled that more reductions would follow, marking the start of an easing cycle. The cut signified the Fed’s confidence that inflation was on a path to its 2% goal, with a recalibration in focus toward ensuring that restrictive monetary policy wouldn’t cause an increase in unemployment. The bond market had largely priced-in the policy shift over the course of the quarter, which saw the U.S. two-year note’s yield dip below the 10-year note’s yield for only the second time since 2022.

There are many read-throughs relative to the Fed’s actions and the market’s subsequent reaction, and from our perspective, there are positives and negatives. On the positive side, we view the steepening of the yield curve as a good sign for our underlying banks and insurance companies who will benefit from higher rates on the long end of the curve. It also increases the expectation that the market will experience a soft landing. The National Bureau of Economic Research (NBER) uses four variables to determine whether the U.S. economy is in recession: Personal Consumption Expenditures (PCE), payrolls, industrial production, and real personal income net of transfer payments. None of these key factors are decreasing, indicating less risk for a possible recession. Additionally, as inflation has decreased, central banks around the world have started to lower their own benchmark interest rates to help prevent excess damage to their own economies. Coordinated global monetary easing has allowed for increased excess liquidity within financial markets and is very favorable for U.S. and global economic growth.

On the negative side, we’re often finding that Fed statements and actions are in stark contrast to what we’re seeing, reading, and expecting during periods where we’d anticipate elevated volatility driven by several factors. Inflation continues to be a significant problem, remaining structurally high even though it has come down on a rate-of-change basis. We don’t think the Fed had justification to cut rates in September, as equity markets and housing prices were at, or near, all-time-highs, and we’re extremely skeptical the market will receive the interest rate cuts that are being priced in over the next year. In Q4 2023, more speculative stocks that would’ve benefited from a lower discount rate rallied materially as upwards of seven cuts were priced in over the course of 2024. There’s been just one so far, and we’ve now seen the same excitement in Q3 2024 from the more speculative pockets of the market that continue to yearn for lower rates, which drove outperformance across equity benchmarks during the quarter. We think the market is too optimistic surrounding the magnitude and overall impact of interest rate cuts in general, and we question the viability of the Fed’s 2% inflation target, given the exploding, runaway federal deficits. For example, while stocks initially rallied on the news of a 50 basis points (bps) rate cut, they’d also go on to rally on the notion that the Fed may not cut too aggressively. Developments like this—where negative situations lead to positive outcomes for equity markets, quickly followed by good news also leading to positive outcomes while the market remains at all-time highs—do not give us great confidence.

Typically, periods when the macroeconomic backdrop is layered with an uncertain U.S. election cycle, war in multiple regions of the world, and curious behavior from the Fed, would lead to significant market volatility. However, what the market has given us is broad-based complacency. So far, the market seems apathetic towards the result of the U.S. election, where the two candidates have signaled their intent to implement vastly different tax policies that will materially impact corporate earnings. While there are certain outcomes of the upcoming election that could usher in a long bull market, a continued political stalemate with an inability to rein in deficits will lead to reaccelerated inflation, no matter who wins the U.S. election in November. This doesn’t appear to be priced in yet, given elevated correlations and limited volatility. Active war in the Middle East and Eastern Europe will tangibly impact economic growth and overall confidence, but the market remains unphased. However, this doesn’t even begin to touch on the simmering geopolitical tensions in Southeast Asia, where most of the global semiconductor capacity is located.

This easing cycle is set to look much different than prior cycles, due to the sticky inflationary backdrop and the fact that the Fed can’t risk a reacceleration in inflation after working for years to bring the year-over-year rate of change down towards more normalized levels. As active managers, this will give us ample opportunity to find stocks trading at prices dislocated from their fundamental values. The investment strategy that excelled during past easing cycles will not be replicated, although the markets are attempting to price that in for at least the short term.

Performance Highlights1

The strategy delivered a solid positive return of 5.62% during Q3 2024, though it lagged the benchmark Russell 2000 Value Index, which returned 10.15%. The underperformance was largely driven by a negative allocation effect, particularly in sectors with higher weightings compared to the benchmark, despite a positive selection effect overall.

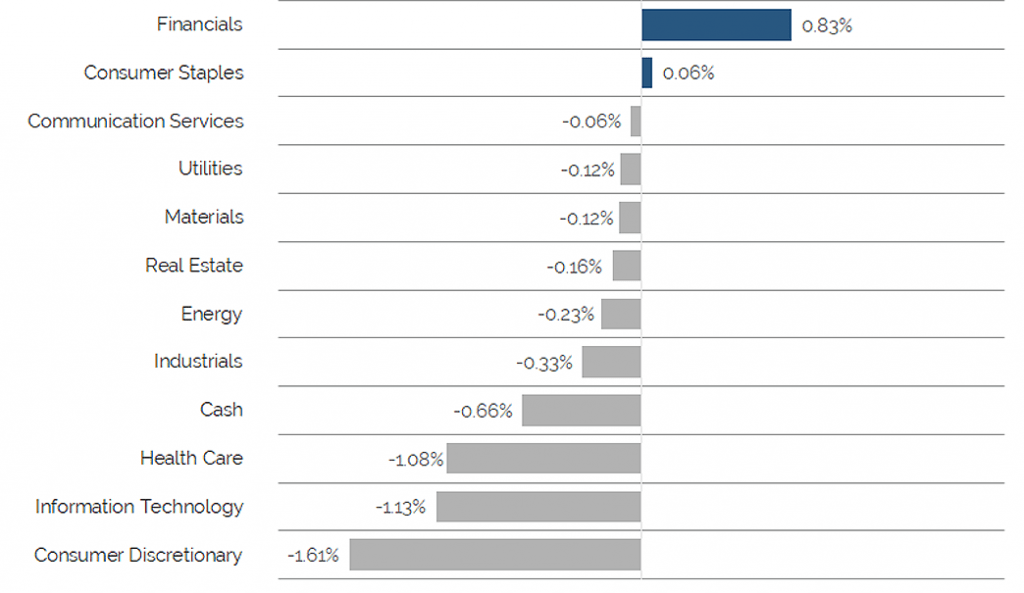

At the sector level, Financials made the strongest contribution to the strategy’s performance, benefiting from both selection and allocation, as stocks within the sector outperformed their peers. Consumer Staples also contributed positively, though the selection effect detracted slightly. However, the strategy’s overweight in Consumer Discretionary, Information Technology, and Health Care negatively impacted returns, with weak stock selection and allocation dragging performance down in these areas. Cash had limited upside in this positive market, as the overall benchmark posted strong returns.

Key individual contributors to the strategy’s performance included Columbia Banking System, Inc. (COLB), Jackson Financial, Inc. (JXN), and Cinemark (CNK), all of which posted strong returns due to positive stock selection within their respective sectors. In contrast, Delek U.S. Holdings, Inc. (DK), Integra Integra LifeSciences (IART), and Silicon Motion Technology Corporation (SIMO) were the biggest detractors, driven by weak performance, particularly in Energy, Health Care, and Information Technology.

In summary, the strategy’s underperformance was mainly due to sector allocation driven by bottom-up stock selection, despite positive results from several strong stock picks.

Performance Attribution2

Top 5 Performance Contributors

| Stock | Avg Weight % | Contribution % (net) |

|---|---|---|

| COLUMBIA BANKING | 3.57 | 1.00 |

| JACKSON FINANCIAL INC-A | 4.21 | 0.95 |

| CINEMARK HOLDING | 3.13 | 0.95 |

| CNO FINANCIAL GR | 3.98 | 0.94 |

| HIGHWOODS PROP | 3.32 | 0.88 |

Columbia Banking System, Inc. (COLB)

In Q3 2024, COLB reported a strong performance. Performance was driven by improving fundamentals, as earnings of $0.67/share came in $0.10 ahead of analyst expectations, highlighting the successes around small-business relationship initiatives as well as cost-saving plans. Net Interest Income (NII) of $428 million exceeded estimates of $420.4 million, aided by accretion income and higher yields on loans. Continued execution around efficiency and strategic deposit growth initiatives supports improved profitability in the near-term. As regional banking industry fundamentals improve with the disinversion of the yield curve, we feel that COLB continues to represent an attractive opportunity within the financial sector.

Jackson Financial, Inc. (JXN)

In Q3 2024, JXN saw a strong stock return, supported by stronger-than-expected capital generation and favorable capital allocation. Adjusted earnings per share (EPS) of $5.32 exceeded estimates of $4.36, reflecting the impact of strong annuity sales. The newly structured hedges that were established in Q1 2024 continue to operate within expectations, allowing for more stable capital generation. This strong capital generation, along with dividend payout and efficient management of the annuity business, provide a solid foundation for continued growth.

JXN offers a compelling investment opportunity with robust growth in annuity sales and efficient capital management. The strong balance sheet and continued focus on operational improvement sets the company up for stable capital generation and consistent capital returns to shareholders. Recent growth in RILA sales provides a natural hedge for the traditional variable annuity business, mitigating market risk and reducing the costs of hedging. Given the company’s solid operational execution and ongoing capital returns, JXN is well positioned to deliver further value to shareholders.

Cinemark Holdings (CNK)

CNK shares positively contributed to performance following the company’s Q2 2024 earnings release, as results delivered a large beat relative to consensus expectations. CNK’s strong results are driven by sustained share gains and healthy ticket pricing levels. The company has solidified its balance sheet and is well positioned for continued earnings expansion as the film release slate normalizes following disruption from the Writers Guild of America strike in 2023.

CNK remains an attractive investment with effective cost management, a recovering box office environment, and expansion of premium offerings. Given the stock’s rise, we have cautiously trimmed our position.

Top 5 Performance Detractors

| Stock | Avg Weight % | Contribution % (net) |

|---|---|---|

| DELEK US HOLDING | 3.12 | -0.93 |

| INTEGRA LIFESCIE | 1.48 | -0.07 |

| SILICON MOTI-ADR | 2.56 | -0.67 |

| ADVANCE AUTO PAR | 1.25 | -0.59 |

| VEREN INC | 2.03 | -0.46 |

Delek US Holdings, Inc. (DK)

DK had a negative impact on performance this quarter. While the company’s refining operations ran well during the quarter, realized margins were weak and the outlook deteriorated as crack spreads compressed during the quarter, primarily due to concerns about lower oil demand in 2025. DK shares were further pressured as the company announced the divestiture of its retail business for a reasonable multiple, but the company didn’t provide an update to investors on the intended use of proceeds from the transaction when the announcement was made in early August. In September, DK announced the Board of Directors approved a substantial increase to its share repurchase authorization.

We maintain an optimistic outlook for DK and have added to our position, reflecting our confidence in the company’s recovery potential despite the recent negative performance. While DK’s refineries have historically posted volatile results, the company recently exceeded cost reduction targets and is expected to detail a new margin improvement plan for its refining operation. DK is taking steps in the right direction by divesting non-core assets, such as the retail business, and enhancing operational efficiency. The current valuation appears favorable, with the company’s market cap trading near the value of DK’s interest in Delek Logistics Partners LP (DKL), suggesting DK’s refining operations are ascribed minimal value. Given the strategic moves towards deconsolidation, DK should be able to return more capital to shareholders, highlighting this disconnect.

Integra LifeSciences (IART)

Integra LifeSciences (IART) detracted during the quarter after resetting guidance lower, partially due to additional compliance spending coupled with a labeling issue that delayed shipment of certain products. The result was an EPS guide that came down nearly $0.50 along with contracting margins. This was a disappointing quarter for IART, as investors were looking for signs indicating the company had moved beyond self-inflicted issues that have dropped shares down towards 10-year lows.

The strategy exited the position early in Q3 given the deterioration in the balance sheet and continued self-inflicted setbacks. Capital was rotated into ideas with a better risk/reward profile.

Silicon Motion Technology (SIMO)

Silicon Motion Technology (SIMO) pulled back during the quarter as investors digested higher go-forward research and development spending in support of future growth, which narrowed near-term EPS estimates, along with broad based pullbacks in smaller-cap Information Technology stocks following a strong first half of the year.

SIMO remains well positioned on a niche part of the semiconductor supply chain and will continue to benefit from long-term growth drivers across data centers, PCs, smartphones, and other devices as customers anticipate the need to support growth that requires higher performance. The company is backed by a clean balance sheet that includes $349 million in cash, no debt, and a dividend yielding 3.3%.

Positioning3

| Stock | Portfolio Weight (%) | Sector |

|---|---|---|

| CNO Financial Group, Inc. | 4.22 | Financials |

| Jackson Financial, Inc. | 4.19 | Financials |

| Columbia Banking System, Inc. | 4.14 | Financials |

| Photronics, Inc. | 3.79 | Information Technology |

| Delek US Holdings, Inc. | 3.73 | Energy |

| FMC Corp | 3.58 | Materials |

| Old National Bancorp/IN | 3.58 | Financials |

| Lincoln National Corp | 3.57 | Financials |

| Comerica, Inc. | 3.44 | Financials |

| Highwoods Properties, Inc. | 3.32 | Real Estate |

| Total | 37.56 |

The strategy’s largest sector overweights are in Consumer Discretionary and Materials, driven by bottom-up stock selection rather than macro views. Additionally, a conservative high-cash allocation is present. The largest underweights are in Real Estate, Utilities, and Health Care, reflecting minimal exposure to these sectors due to stock selection choices.

Within the strategy, Financials is the largest sector, consisting of multiple holdings, followed by Consumer Discretionary and Materials. Financials maintains a high allocation with several significant positions, while sectors like Real Estate and Health Care are notably underrepresented. The strategy’s allocation reflects the focus on stock picking rather than targeting specific sectors based on macro trends.

Significant stock positions include CNO Financial Group, Inc., Jackson Financial, Inc., Columbia Banking System, Inc., and Old National Bancorp within the Financials sector. Other prominent names are Photronics, Inc., from Information Technology, Delek US Holdings, Inc., in Energy, and FMC Corporation in Materials. The top 10 holdings comprise 37.56% of the total strategy, illustrating a concentrated approach in key stocks.

In summary, the sector exposure results from the bottom-up stock picking strategy and doesn’t reflect any particular macroeconomic view. The strategy remains diversified across selected sectors with targeted stock positions driving overall allocation.

Outlook

Looking ahead to Q4 2024, we see continued opportunities to populate our strategy with great companies and to identify stocks trading at discounted levels, especially as correlations remain high across the equity market universe. The valuation gap between large-cap and small-cap stocks remains at historically elevated levels, with the Snow Small Cap Value Strategy trading at 9x forward earnings and the Russell 2000 Value index trading at 11x forward earnings compared to 20x for the S&P 500, signaling a significant discount.

We remain confident in the stocks we’re buying and continue to find great value and opportunities while populating our strategy, but would welcome a pullback in more frothy pockets of the market to better align with investor expectations. We have a positive outlook on the Energy sector, as current world events are threatening oil supplies and as the U.S. works to refill strategic petroleum reserves that are near historical lows. We’re also optimistic about the banks and insurance companies in the strategy that would stand to benefit from a steepening yield curve. Declining recessionary risks as well as global monetary easing lay the groundwork for what could be an improved earnings trajectory for areas of the market that haven’t seen the same multiple expansion as mega-cap tech or perceived artificial intelligence (AI) beneficiaries.

Our positioning is solely a function of stock selection, as valuation levels for these stocks continue to discount a perceived recession. As a soft landing has become the collective expectation, we feel the strategy will see considerable mean-reversion. Mean-reversions are often fast, but can have long-lasting implications for relative performance. An example of this happened this past July after the release of the June consumer price index (CPI) report. On that day, the NASDAQ fell by 2% and the Russell 2000 Small Cap Index rose by 3.6%—representing the largest single-day outperformance by small cap in over 40 years. While this was only one day, it highlights how quickly markets can adjust to even the slightest change in perceived economic trajectory, and exemplifies the differentiated return stream that small caps can have relative to larger cap, growth-oriented peers.

In managing the Easterly Snow Small Cap Value Strategy, we remain laser-focused on populating our strategy with companies featuring great balance sheets, real free-cash-flows, stock-specific catalysts, and a path towards a normalized earnings recovery—which will ultimately lead to a price-to-earnings (P/E) re-rating. While the visible uncertainties today seem to stand in contrast to the market’s steady climb, Snow’s research team remains agile and eager to continue being an effective steward of capital no matter the macroeconomic or geopolitical backdrop.

Source: SEI Global Services as September 30, 2024

1Securities shown represent the largest contributors and detractors to the portfolio’s performance for the period and do not represent all holdings within the portfolio. There is no guarantee that such holdings are currently or will remain in the portfolio. For a complete list of holdings and an explanation of the methodology employed to determine this information, please contact Easterly. This information is not to be construed as an offer to buy or sell any financial instrument nor does it constitute an offer or invitation to invest in any fund managed by Easterly and has not been prepared in connection with any such offer.

2Performance shown is the Easterly Investment Partners LLC (“the Firm”) Snow Small Cap Value composite in USD. Past performance is not indicative of future results. Gross performance results do not include advisory fees and other expenses an investor may incur, which when deducted will reduce returns. Changes in exchange rates may have adverse effects. Net performance results reflect the application of a model investment management fee which is higher than the actual average weighted management fee charged to accounts in the composite applied to gross performance results. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. The Firm claims compliance with the GIPS® standards; this information is supplemental to the GIPS® report included in this material. Returns greater than one year are annualized

3References to securities, transactions or holdings should not be considered a recommendation to purchase or sell a particular security and there is no assurance that, as of the date of publication, the securities remain in the portfolio. Additionally, it is noted that the securities or transactions referenced do not represent all of the securities purchased, sold or recommended during the period referenced and there is no guarantee as to the future profitability of the securities identified and discussed herein. Top ten holdings information shown combines share listings from the same issuer, and related depositary receipts, into a singular holding to accurately present aggregate economic interest in the referenced company.

Trailing Performance (%)

as of September 30, 2024

| QTD | YTD | 1-Year | 3-Year | 5-Year | 7-Year | 10-Year | Since Inception* | |

|---|---|---|---|---|---|---|---|---|

| Composite (gross) | 5.62 | 14.94 | 29.50 | 10.34 | 18.04 | 12.00 | 8.93 | 9.96 |

| Composite (net) | 5.43 | 14.34 | 28.60 | 9.58 | 17.22 | 11.22 | 8.18 | 9.20 |

| Russell 2000 Value | 10.15 | 9.22 | 25.88 | 3.77 | 9.28 | 6.59 | 8.22 | 6.57 |

Calendar Year Performance (%)

| 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Composite (gross) | 22.51 | -6.68 | 28.44 | 24.16 | 19.39 | -18.81 | 8.35 | 22.75 | -15.99 | 4.92 |

| Composite (net) | 21.66 | -7.33 | 27.56 | 23.31 | 18.57 | -19.39 | 7.60 | 21.91 | -16.59 | 4.19 |

| Russell 2000 Value | 14.65 | -14.48 | 28.27 | 4.63 | 22.39 | -12.86 | 7.84 | 31.74 | -7.47 | 4.22 |

Source: SEI Global Services

*Inception: 10/31/06

Performance shown is the Easterly Investment Partners LLC (“the Firm”) Snow Small Cap Value composite in USD. Past performance is not indicative of future results. Gross performance results do not include advisory fees and other expenses an investor may incur, which when deducted will reduce returns. Changes in exchange rates may have adverse effects. Net performance results reflect the application of a model investment management fee which is higher than the actual average weighted management fee charged to accounts in the composite applied to gross performance results. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. The Firm claims compliance with the GIPS® standards; this information is supplemental to the GIPS® report included in this material. Returns greater than one year are annualized.

Attribution vs Russell 2000 Value

Source: Bloomberg

Source: Bloomberg

Holdings, sector weightings, market capitalization and portfolio characteristics are subject to change at any time and are based on a representative portfolio, and may differ, sometimes significantly, from individual client portfolios.

GIPS® Report

Easterly Investment Partners LLC Snow Snow Small Cap Value Composite

Composite Inception Date: October 31, 2006

Composite Creation Date: 07/01/2021

| Year End | Composite Performance | Annualized 3-Year Standard Deviation | Total Assets (millions) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Gross | Net | Russell 2000 Value | Composite | Russell 2000 Value | Composite Dispersion | Total Firm Assets | Firm (AUM) | Firm (AUA)* | Composite | Number of Accounts | |

| 2023 | 22.51% | 21.66% | 14.65% | 24.00% | 22.06% | N/A | 1,730 | 1,090 | 640 | 64 | Five or fewer |

| 2022 | -6.68% | -7.33% | -14.48% | 33.38% | 27.66% | N/A | 1,834 | 1,341 | 493 | 55 | Five or fewer |

| 2021 | 28.44% | 27.56% | 28.27% | 32.10% | 25.35% | N/A | 2718 | 1540 | 1178 | 77 | Five or fewer |

| 2020 | 24.16% | 23.31% | 4.63% | 32.68% | 26.12% | 0.10% | - | - | 78 | Five or fewer | |

| 2019 | 19.39% | 18.57% | 22.39% | 20.50% | 15.70% | 0.20% | - | - | 82 | Five or fewer | |

| 2018 | -18.81% | -19.39% | -12.86% | 20.10% | 15.80% | N/A | - | - | 103 | Five or fewer | |

| 2017 | 8.35% | 7.60% | 7.84% | 18.20% | 14.00% | N/A | - | - | 421 | 6 | |

| 2016 | 22.75% | 21.91% | 31.74% | 18.40% | 15.50% | 0.60% | - | - | 627 | 10 | |

| 2015 | -15.99% | -16.59% | -7.47% | 15.00% | 13.50% | 0.50% | - | - | 643 | 12 | |

| 2014 | 4.92% | 4.19% | 4.22% | 15.20% | 12.80% | N/A | - | - | 557 | 9 | |

*Firm-wide advisory- only assets. Assets under Advisement (AUA) includes the assets where Easterly Investment Partners (“Easterly”) provides its advisory services in similar strategies and does not have discretionary trading authority.

Firm Definition

For purposes of complying with the GIPS® standards, the firm is defined as Easterly Investment Partners LLC (“EIP”) which is an SEC registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, effective January 2019. The firm was redefined on 1/1/2023 to reflect that EIP is comprised of two distinct firms: the institutional asset management operations, investment strategies, performance track records, certain employees and client accounts of Levin Capital Strategies, which were acquired by EIP in March 2019, and Snow Capital Management LLC’s (“SCM”) asset management business, investment strategies, performance track records, client accounts, and certain employees, acquired by EIP in July 2021.

Firm Verification Statement

Easterly claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Easterly has been independently verified for the period April 1, 2019 through December 31, 2023. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis.

Composite Verification Statement

The Small Cap Value Composite has had a performance examination from composite inception date through December 31, 2023. The verification and performance examination reports are available upon request.

Composite Description

The Small Cap composite provides exposure to long-only US publicly-listed securities and ADRs, and may occasionally invest in convertible and corporate bonds, taking into account various factors. The strategy is biased toward Small capitalization value stocks, and position sizes range between 0.5% to 5%, with liquidity as a consideration.

Benchmark Description

The Russell 2000 Value Index measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. Indexes are unmanaged. It is not possible to invest directly in an index.

Performance Calculation

All returns are calculated and presented in US dollars based on fully discretionary AUM, including those investors no longer with the firm. All gross composite returns are net of transaction costs and foreign withholding taxes, if any, and reflect the reinvestment of interest income and other earnings. Net performance results reflect the application of a model investment management fee which is higher than the actual average weighted management fee charged to accounts in the composite applied to gross performance results. Composite net returns are calculated by reducing daily gross returns by an amount where the monthly net return will be the monthly gross return reduced by 1/12th of the highest advisory fee rate. Monthly net returns are then geometrically linked to calculate the annual net return. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. Actual investment advisory fees incurred by clients will vary. Policies for valuing investments, calculating performance, and preparing GIPS reports are available upon request. A list of composite descriptions and a list of broad distribution pooled funds are available upon request. Past performance is not indicative of future performance. Results may be higher or lower based on IPO eligibility, and actual investor’s returns may differ, depending upon date(s) of investment(s). Additional information is available upon request. The Small Cap Value Composite has removes accounts from the composite for the period of significant cash flow of greater than or equal to $20 million.

Investment Management Fee Schedule

The current standard management fee schedule for a segregated account managed to the composite strategy is as follows: 0.70% on the first $25 million; 0.55% on the next $75 million; 0.50% on the next $100 million; 0.45% on the next $100 million; 0.35% on the balance.

Composite Dispersion

The annual composite dispersion, if shown, is an asset-weighted standard deviation calculated using gross returns for the accounts in the composite the entire year. The internal dispersion measure is not applicable if there are five or fewer portfolios in the composite for the entire year if that is the reason this is N/A.

Standard Deviation

The annualized 3-year standard deviation represents the annualized standard deviation of actual gross composite and benchmark returns, using the rolling 36 months ended each year end. Standard deviation is a measurement of historical volatility of investment returns.

Trademark

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

Important Disclosures

© 2024. Easterly Asset Management. All rights reserved.

Easterly Asset Management’s advisory affiliates (collectively, “EAM” or “the Firm”), including Easterly Investment Partners LLC, Easterly Funds LLC, and Easterly EAB Risk Solutions LLC (“Easterly EAB”) are registered with the SEC as investment advisers under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about the firm, including its investment strategies and objectives, can be found in each affiliate’s Form ADV Part 2 which is available on the www.sec.gov website. This information has been prepared solely for the use of the intended recipients; it may not be reproduced or disseminated, in whole or in part, without the prior written consent of EAM.

No funds or investment services described herein are offered or will be sold in any jurisdiction in which such an offer or sale would be unlawful under the laws of such jurisdiction. No such fund or service is offered or will be sold in any jurisdiction in which registration, licensing, qualification, filing or notification would be required unless such registration, license, qualification, filing, or notification has been affected.

The material contains information regarding the investment approach described herein and is not a complete description of the investment objectives, risks, policies, guidelines or portfolio management and research that supports this investment approach. Any decision to engage the Firm should be based upon a review of the terms of the prospectus, offering documents or investment management agreement, as applicable, and the specific investment objectives, policies and guidelines that apply under the terms of such agreement. There is no guarantee investment objectives will be met. The investment process may change over time. The characteristics set forth are intended as a general illustration of some of the criteria the strategy team considers in selecting securities for client portfolios. Client portfolios are managed according to mutually agreed upon investment guidelines. No investment strategy or risk management techniques can guarantee returns or eliminate risk in any market environment. All information in this communication has been obtained from sources believed to be reliable but cannot be guaranteed. Investment products are not FDIC insured and may lose value.

Investments are subject to market risk, including the loss of principal. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate. The information contained herein does not consider any investor’s investment objectives, particular needs, or financial situation and the investment strategies described may not be suitable for all investors. Individual investment decisions should be discussed with a personal financial advisor.

Any opinions, projections and estimates constitute the judgment of the portfolio managers as of the date of this material, may not align with the Firm’s opinion or trading strategies, and may differ from other research analysts’ opinions and investment outlook. The information herein is subject to change without notice and may be superseded by subsequent market events or for other reasons. EAM assumes no obligation to update the information herein.

References to securities, transactions or holdings should not be considered a recommendation to purchase or sell a particular security and there is no assurance that, as of the date of publication, the securities remain in the portfolio. Additionally, it is noted that the securities or transactions referenced do not represent all of the securities purchased, sold or recommended during the period referenced and there is no guarantee as to the future profitability of the securities identified and discussed herein. As a reminder, investment return and principal value will fluctuate.

The indices cited are, generally, widely accepted benchmarks for investment performance within their relevant regions, sectors or asset classes, and represent non managed investment portfolio. It is not possible to invest directly in an index.

This communication may contain forward-looking statements, which reflect the views of EAM and/or its affiliates. These forward-looking statements can be identified by reference to words such as “believe”, “expect”, “potential”, “continue”, “may”, “will”, “should”, “seek”, “approximately”, “predict”, “intend”, “plan”, “estimate”, “anticipate” or other comparable words. These forward-looking statements or other predications or assumptions are subject to various risks, uncertainties, and assumptions. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. Should any assumptions underlying the forward-looking statements contained herein prove to be incorrect, the actual outcome or results may differ materially from outcomes or results projected in these statements. EAM does not undertake any obligation to update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by applicable law or regulation.

Past performance is no guarantee of future results.

20241023-3961718